Futures: Overnight, LME copper opened at $9,998/mt, touched a low of $9,989/mt, and rose to a high of $10,130/mt before closing at $10,094.5/mt. The overall trend initially fluctuated at low levels before surging significantly, pulling back after reaching the high. The increase was 1.61%, with a trading volume of 18,300 lots and open interest of 301,000 lots. Overnight, the most-traded SHFE copper 2505 contract opened at 81,960 yuan/mt, touched a low of 81,910 yuan/mt, and rose to a high of 82,820 yuan/mt before closing at 82,780 yuan/mt. The overall trend initially declined before rebounding sharply and continuing to rise. The increase was 1.3%, with a trading volume of 60,800 lots and open interest of 254,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) COMEX copper hit a record high as the market expects Trump to impose high import tariffs on copper.

On Tuesday EST, COMEX copper futures rose more than 2.3% intraday, hitting a record high of $5.2105 per pound, surpassing the previous record of $5.199 set on May 20 last year.

(2) To revitalize the US shipbuilding industry, US President Trump previously proposed a self-defeating idea to charge docking fees for all fleets that dock at US ports and are built in China or fly the Chinese flag. At a public hearing held by the US Trade Representative (USTR) on the fee issue, many US ship industry executives stated that Trump's move would backfire, harming US domestic ship operators, seaports, exporters, and impacting US agriculture, manufacturing, mining, and other industries.

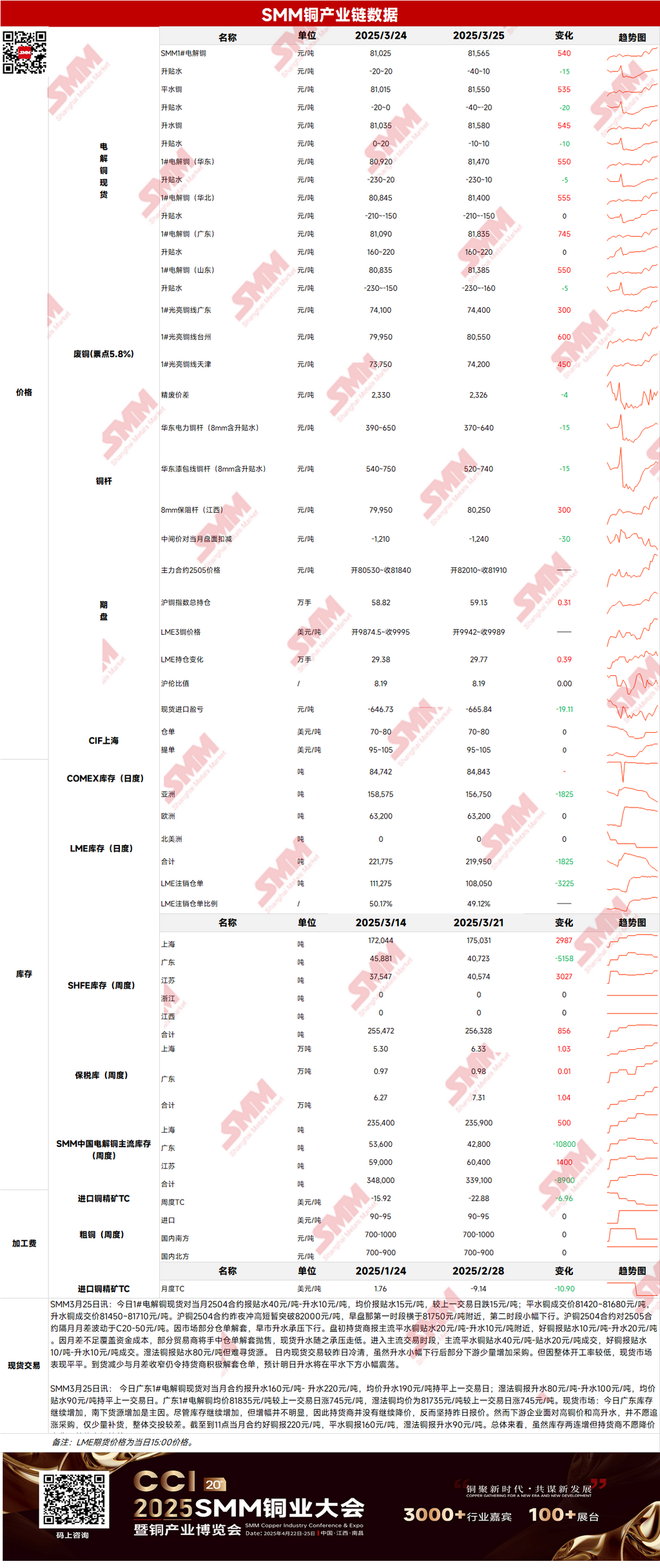

Spot: (1) Shanghai: On March 25, spot #1 copper cathode against the front-month 2504 contract was quoted at a discount of 40 yuan/mt to a premium of 10 yuan/mt, with an average discount of 15 yuan/mt, down 15 yuan/mt MoM. Spot trading was quieter than the previous day, with some downstream buyers increasing purchases slightly after the premium declined. However, due to the low overall operating rate, the spot market showed mediocre performance. Reduced arrivals and narrowing price spreads between futures contracts still prompted suppliers to actively unwind warrants. Spot premiums are expected to fluctuate slightly below parity today.

(2) Guangdong: On March 25, spot #1 copper cathode in Guangdong against the front-month contract was quoted at a premium of 160-220 yuan/mt, with an average premium of 190 yuan/mt, flat MoM. Overall, although inventories increased for two consecutive days, suppliers were unwilling to lower prices, resulting in poor trading.

(3) Imported copper: On March 25, warrant prices were $70-80/mt, QP April, with the average price flat MoM; B/L prices were $95-105/mt, QP April, with the average price flat MoM; EQ copper (CIF B/L) was $40-50/mt, QP April, with the average price flat MoM. Quotations referred to cargoes arriving in mid-to-late March and early April. Market offers increased MoM, but buyers remained cautious due to the unresolved US tariff decision next week, resulting in limited actual transactions. It was heard that EQ offers continued to surge, with a significant reduction in African cargoes arriving in April.

(4) Secondary copper: On March 25, secondary copper raw material prices rose 300 yuan/mt MoM. Bare bright copper prices in Guangdong were 74,300-74,500 yuan/mt, up 300 yuan/mt from the previous day. The price difference between primary metal and scrap was 2,326 yuan/mt, down 4 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,745 yuan/mt. According to the SMM survey, as copper prices hover at highs, traders and secondary copper rod enterprises had no opportunity to sell after hedging, so some secondary copper rod enterprises had to close futures positions and sell secondary copper rods at low prices in the market to quickly recover funds to meet raw material procurement needs.

(5) Inventories: On March 25, LME copper cathode inventories decreased by 1,825 mt to 219,950 mt; on March 25, SHFE warrant inventories decreased by 2,871 mt to 143,140 mt.

Prices: On the macro front, as Trump considers a "two-step" strategy for new tariff policies, market concerns about trade policy uncertainty intensified, coupled with a decline in the US consumer confidence index to its lowest level since February 2021, the US dollar index fell, benefiting copper prices. On the supply side, as some warrants were unwound, suppliers sold off, increasing spot copper cathode supply and putting pressure on spot premiums. On the demand side, although downstream purchases increased slightly after the premium declined, the overall operating rate remained low, resulting in mediocre performance in the spot market. Price-wise, despite favorable macro factors, insufficient fundamental demand limited the upside, and copper prices are expected to fluctuate rangebound today.

》Click to view the SMM Metals Database

[The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct investment research decision-making advice. Clients should make decisions cautiously and not use this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]